What has happened since last month? As of mid-September 2025, the North American lumber market shows mixed signals. Futures prices remain relatively supported near $570–$585, while spot and composite indices are weakening. U.S. housing starts have cooled, and Canadian producers are under pressure from profitability constraints. Trade-related measures remain part of the backdrop but without a clear directional tilt. Below is a structured update of the most recent lumber forecast, enhanced with additional context and data.

Market Snapshot – Mid-September 2025

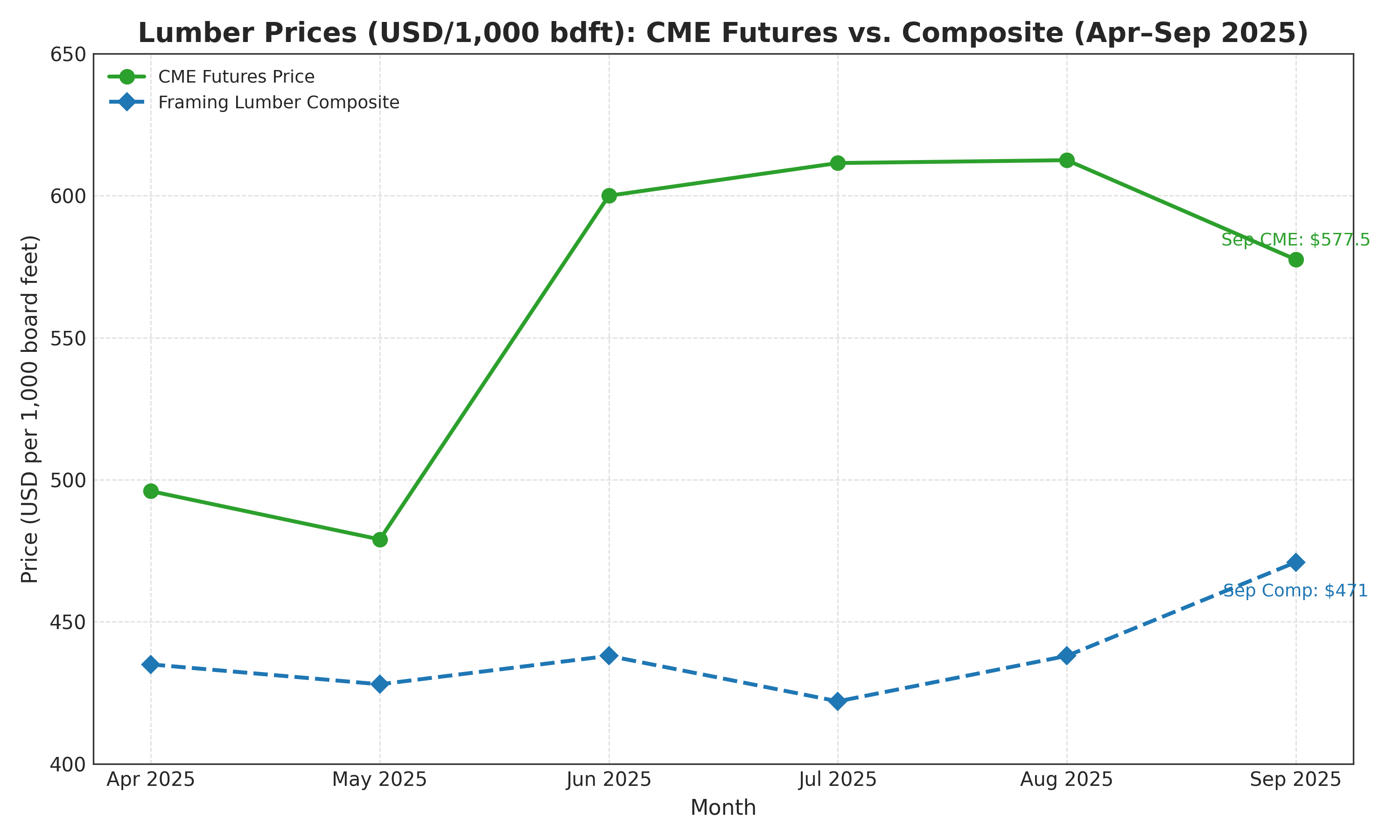

- Framing Lumber Composite / Spot Indices: The Madison framing index is ~$471, representing a ~12% decline month-over-month. The NAHB framing composite shows comparable downward pressure.

- CME Lumber Futures: Near-term contract prices are in the $570–$585 range per 1,000 board feet, reflecting current positioning in the futures market.

- Futures Volume & Open Interest: Recent data suggests moderate volume and open interest, lower than during the peak August run-up, pointing to cautious market participation.

- Producer Price Index (PPI): Lumber-related segments have shown easing cost pressures in upstream materials and inputs over recent months.

Key Market Drivers for this Lumber Forecast

1. Composite & Spot Price Momentum

The divergence between futures and spot markets is noteworthy. Spot/composite indices are decelerating, reflecting real-time demand softening. Futures remain somewhat insulated by expectations of supply constraints or delayed reactions to fundamentals.

2. Futures Market Liquidity & Positioning

Volume and open interest in recent weeks have declined from August peaks. This suggests that many speculative participants are stepping back, awaiting clearer signals from the demand side.

3. Upstream Cost Pressures and PPI Trends

Input cost inflation, as measured by PPI components, has softened in lumber-related categories. This provides slight relief to producers already operating under tightening margins.

4. Housing Starts and Demand Sentiment

August housing starts in the U.S. recorded ~1.307 million SAAR, down ~8.5% from July, with single-family starts dropping ~7%. Lower starts portend weakening demand if trends continue into the fall.

5. Producer Margins & Mill Behavior

Many Canadian producers are operating below or near break-even thresholds (estimated around $600 per 1,000 board feet), prompting curtailments or cautious restarts. This creates an asymmetry: downside risk is somewhat capped, but upside gains may require stronger demand to justify higher prices.

6. Trade Measures & Policy Environment

Trade measures (countervailing, anti-dumping) on Canadian lumber remain in force, with combined rates reportedly reaching up to ~35%. Meanwhile, the possibility of a Section 232 review remains under consideration as a wildcard. These parameters provide context and risk but do not favor a directional bias.

North American Lumber Market – September 2025 Indicator Table

| Indicator | Mid-Sep Value / Estimate | Recent Change | Outlook / Projection |

|---|---|---|---|

| CME Lumber Futures (near-term) | $570–$585 / 1,000 bdft | Higher vs August benchmarks | Supported short-term; downside risk if demand weakens. |

| Spot / Composite Lumber (Madison / NAHB) | $470–480 | ~ –12% MoM | Likely gradual declines unless demand rebounds. |

| U.S. Housing Starts (Aug SAAR) | 1.307 million | –8.5% MoM | Trend may carry into Q4 if sentiment stays weak. |

| Canadian Producer Break-even | ~ $600 / 1,000 bdft | Spot below threshold | Further curtailments likely if price fails to recover. |

| Futures Volume & Open Interest | Moderate / declining | Lower than August highs | Reduced speculative leverage; more reliance on fundamentals. |

| Producer Price Index (PPI) – Lumber inputs | Easing slightly | Downward trend from mid-2025 peaks | Moderate input relief could support margins in near term. |

Outlook For Late 2025 and Early 2026

Given current data, there are multiple plausible scenarios:

- Base case (stabilization / mild softening): Futures and spot converge in a downward drift, with prices holding in a broad $500–$600 band if demand stabilizes.

- Downside scenario: Housing starts weaken further; spot prices bleed; producers curtail more aggressively; futures slip toward $450–$550 territory.

- Upside rebound (less likely): Unexpected strength in homebuilding, sudden repair demand, or supply disruptions push both spot and futures higher.

Sources & References

- CME Group – Lumber Market Overview (mid-2025 futures pricing)

- Investing.com – Historical lumber futures data

- TradingEconomics – Current commodity lumber price series

- NAHB – Framing lumber composite / price reports

- Newswire / press releases – lumber price + housing starts updates

- Bloomberg et al. – commentary on trade measures, duties, cost pressures

- FRED / U.S. Bureau of Labor Statistics – PPI data for lumber inputs

- Company, industry, and mill reports on curtailments and margins