As of early July 2025, the lumber forecast indicates that lumber prices across North America remain stable following a gradual softening trend. Construction demand remains slow, while production continues to be limited by seasonal downtime and reduced capacity. Traders and producers are monitoring conditions closely as the industry enters the peak summer season.

📉 Market Snapshot – Early July 2025

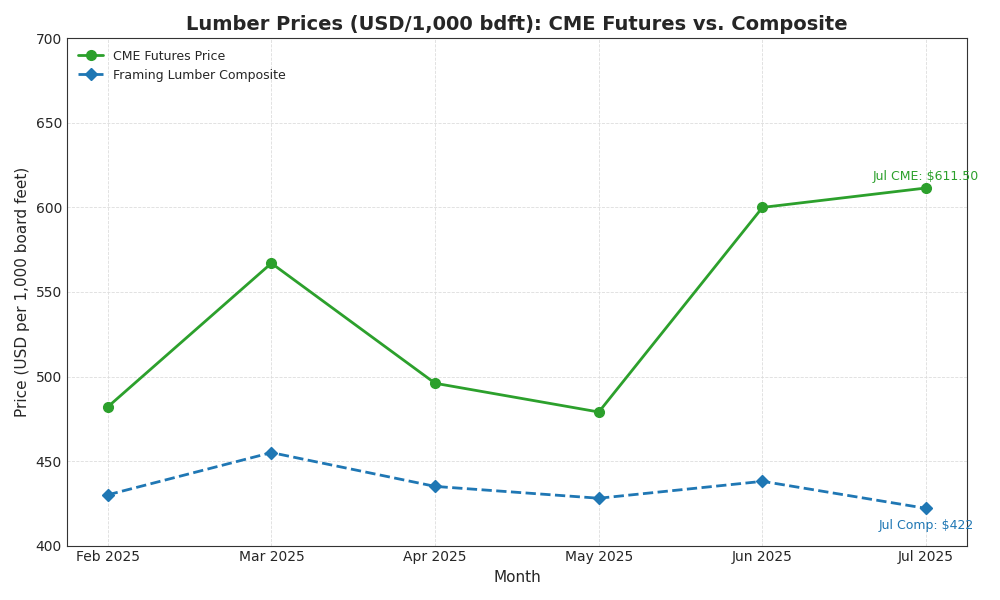

- Framing Lumber Composite: $422 per 1,000 bdft (as of July 4) – down $16 from June, and the lowest since October 2024. Despite the drop, prices remain up 16.6% year-over-year.

- CME Lumber Futures: $607.03 per 1,000 bdft (July 8 closing) – down 0.42% from the prior session but up 0.7% over the past 30 days.

- Futures Market Volume: Approximately 1,433 contracts traded on July 8, with open interest at 7,148 (down 26 contracts from the prior session).

Key Market Drivers

1. Supply and Production Trends

North American lumber output declined 2.1% year-over-year in Q1 2025, with total production reaching just over 9.1 billion board feet. Imports into the U.S. also slowed, down roughly 5.1%, including a 6.5% drop in Canadian shipments. Planned summer maintenance and previous curtailments continue to restrict mill output.

2. Construction Demand

High mortgage rates are still limiting new housing starts. Builders remain cautious, keeping inventories light and purchasing mainly to meet short-term demand. Housing permits and starts remain below pre-2023 levels, contributing to slower lumber consumption in most U.S. markets.

3. Seasonal & Environmental Conditions

With wildfire season underway, logging and shipping operations in the western U.S. and Canada face localized delays, though no widespread disruptions have been reported. Hot weather in southern regions has also affected logging hours and hauling schedules.

4. Market Activity and Futures

Open interest in lumber futures remains relatively low, reflecting limited speculative or hedge-driven activity. As of early July, 2025 futures contracts showed modest gains, but market momentum remains weak. Historically, prices begin to firm up in late summer, particularly as Q3 inventory needs rise.

📊 North American Lumber Market – July 2025

| Indicator | Value (as of July 5–8, 2025) | Change from June 2025 | Change from July 2024 |

|---|---|---|---|

| Framing Lumber Composite | $422 per 1,000 bdft | ▼ $16 (−3.7%) | ▲ $60 (+16.6%) |

| CME Futures (July contract) | $607.03 per 1,000 bdft | ▲ $4.41 (+0.7%) | ▲ ~$125 (+~26%) |

| Futures Volume (July 8) | 1,433 contracts | ▼ 106 contracts | N/A |

| Open Interest (July 8) | 7,148 contracts | ▼ 26 contracts | N/A |

| North American Production (Q1) | ~9.1 bbf | ▼ 2.1% YoY | ▼ 2.1% YoY |

| Housing Starts | Below historical average | Flat | ▼ ~9–10% est. |

| Environmental Conditions | Wildfire risk moderate in West | Seasonally elevated | Normal range |

Looking Ahead

Market watchers expect lumber prices to hold relatively steady through late July. Supply remains tight due to mill reductions and slow import recovery, while construction activity remains constrained. As seasonal production increases in August and wildfire risk stabilizes, pricing may begin to trend upward into Q4.

See how this report compares with last month’s.

Sources and References

- Framing Lumber Composite: NAHB Weekly Lumber Price Index – July 4, 2025

- CME Futures Data: TradingEconomics – Lumber Futures Quotes – July 8, 2025

- Market Volume: AP Market Brief – Lumber Futures Activity – July 8, 2025

- Production Figures: NAHB Housing & Economic Data – Q1 2025 Update

- Open Interest Trends: Coshocton Grain Market Insight – May–July 2025

- Seasonal Wildfire Conditions: Fastmarkets Forestry Outlook – July 2025

- Year-over-Year Analysis: CalculatedRisk Blog – July 7, 2025